Monday, 15 June 2026 12:30 PM

Company Update

ARLINGTON, TX / ACCESS Newswire / June 15, 2026 / Small businesses across the United States are entering 2026 with a level of tax certainty not seen in years, thanks to permanent provisions established under recent federal tax legislation. According to JTC CPAs, these changes are creating new opportunities for business owners to strengthen cash flow, invest in growth, and improve long-term financial planning.

Among the most significant developments are the permanent extension of the Qualified Business Income (QBI) deduction, the restoration of 100% bonus depreciation, expanded equipment expensing opportunities, and updated rules affecting Qualified Small Business Stock (QSBS), research and development deductions, and multi-state tax compliance.

"Business owners now have a stronger foundation for long-term planning," said Jack Trent, founding partner of JTC CPAs. "The permanence of several major tax provisions allows companies to make investment decisions with greater confidence while reducing uncertainty around future tax obligations."

Permanent QBI Deduction Creates Long-Term Planning Opportunities

One of the most impactful changes for pass-through entities is the permanent extension of the Section 199A Qualified Business Income deduction. Eligible sole proprietorships, partnerships, and S corporations can continue deducting up to 20% of qualified business income, potentially reducing federal tax liability by thousands of dollars annually.

The permanence of this deduction allows business owners to implement multi-year tax strategies without concerns about the provision expiring.

Full Bonus Depreciation Encourages Business Investment

Businesses purchasing qualified assets after January 19, 2025, can once again benefit from permanent 100% first-year bonus depreciation. The provision allows companies to immediately deduct the full cost of eligible property rather than depreciating expenses over several years.

Qualified assets include:

Manufacturing and production equipment

Business-use vehicles

Computer hardware and software

Certain commercial property improvements

Eligible production facilities meeting construction requirements

The provision is expected to improve cash flow and encourage expansion projects nationwide.

Research and Development Expenses Become Immediately Deductible

Technology companies, manufacturers, and innovation-driven businesses also received favorable treatment through the restoration of immediate deductions for qualifying domestic research and development expenses.

The change reverses previous capitalization requirements and enables companies to recognize tax benefits sooner, improving liquidity and encouraging continued innovation.

Tax professionals emphasize the importance of maintaining detailed documentation to substantiate qualifying R&D activities and related expenditures.

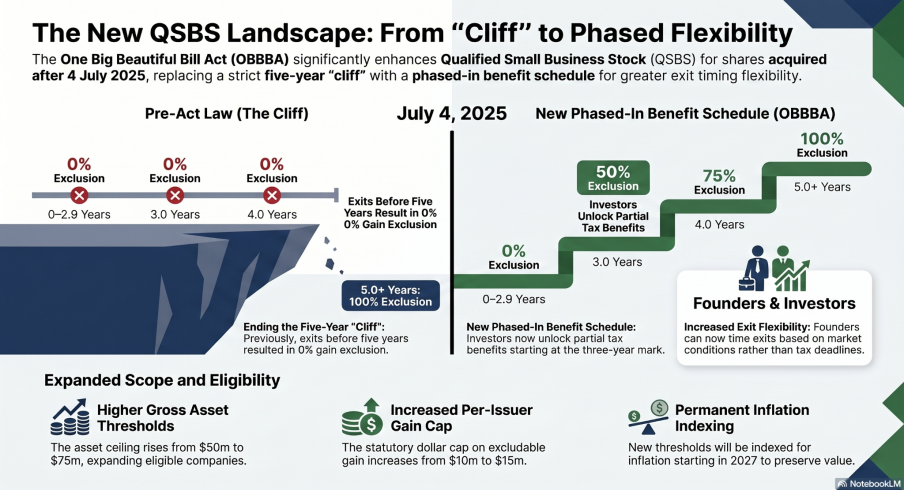

Updated QSBS Rules Provide Greater Flexibility for Founders and Investors

The legislation also introduces a new tiered exclusion schedule for Qualified Small Business Stock acquired after July 4, 2025.

Under the revised framework:

Less than 3 years: No exclusion

3 years: 50% gain exclusion

4 years: 75% gain exclusion

5 years or more: 100% gain exclusion

Additionally, the QSBS gain exclusion cap increased from $10 million to $15 million, while the gross asset limitation rose from $50 million to $75 million, both indexed for inflation.

Industry experts believe these changes could encourage entrepreneurship and increase investment in growing businesses.

Multi-State Businesses Face Ongoing Nexus Compliance Challenges

Despite federal tax simplification, companies operating across multiple states continue to face evolving economic nexus requirements.

Businesses selling products or services in multiple jurisdictions must monitor state-specific sales thresholds, register when required, and remain aware of "trailing nexus" provisions that may extend collection obligations beyond the year a threshold is exceeded.

JTC CPAs recommends that growing businesses, including those operating in markets such as Boise and other growing business hubs across the country, regularly review sales activity by state to avoid compliance risks and unexpected penalties.

International Tax Rules Continue to Evolve

Businesses with foreign subsidiaries should also evaluate recent international tax changes, including the transition from Global Intangible Low-Taxed Income (GILTI) to Net CFC Tested Income (NCTI).

The revised framework permanently establishes a 40% deduction while eliminating the previous deemed tangible income return calculation. These modifications may significantly affect tax modeling, acquisitions, ownership restructuring, and international expansion strategies.

How Accounting & Tax Services Are Changing and Why Businesses Still Need Them

Accounting and tax services advance alongside technology; however, their core role stays the same. Undoubtedly, AI can efficiently process large volumes of data and automate routine tasks, but it cannot replace the judgment, context, and client trust that lie at the heart of professional accounting work.

Currently, fewer individuals are starting careers in accounting due to concerns about automation. But the thing to understand is that the profession is not being replaced; it is being enhanced. AI is a tool that removes repetitive, time-consuming work and allows accountants and tax professionals to focus more on advisory services, tax strategy, and business planning.

Rather than reducing the need for professionals, this shift offers new opportunities for the role of financial specialists. The work is progressing from entirely compliance-based tasks to higher-value decision-making support for businesses.

In the long run, the accounting profession cannot be replaced by AI. While AI handles routine tasks, humans can focus on strategic work.

Looking Ahead

With permanent tax provisions now in place, 2026 offers a rare opportunity for small businesses to develop long-term financial strategies with greater certainty. Companies that proactively leverage available deductions, investment incentives, and compliance planning may be better positioned to strengthen profitability and pursue sustainable growth.

About JTC CPAs

JTC CPAs provides accounting, tax planning, business advisory, and financial consulting services to businesses and individuals throughout the United States. The firm helps clients navigate complex tax regulations, improve financial performance, and develop strategies for long-term success.

Contact Information:

Company Name: JTC CPAs

Contact Persons: Jack Trent

Website: https://www.jtccpas.com/

Email: [email protected]

SOURCE: JTC CPAs